NVT Signal, or Bitcoin’s “PE Ratio”, is one of the best metrics for identifying over-valuation. However, the drastically changing nature of the Bitcoin network, and movement off-chain, could make traditionally high NVT Signal values relatively less expensive in the future. Using a Dynamic Range NVT Signal allows for continued maturity in the Bitcoin network and ongoing identification of relative over- and under-valuation.

What is “NVT Signal?

NVT Signal (credit: to Willy Woo and Dmitry Kalichkin) is akin to a “PE ratio” for Bitcoin. It can be used to identify when Bitcoin is overbought (expensive) or oversold (cheap). It does this by calculating the ratio of Bitcoin’s market capitalization to its daily on-chain transaction value. The power of NVT is in its ability to put a price against the value that the Bitcoin Network delivers — secure, immutable transactions.

As defined by Dmitry, NVT Signal is calculated as follows:

NVT Signal = Circulating Market Cap / 90 Average On-Chain Transaction Value

However, just having the NVT Signal value isn’t enough. What level indicates Bitcoin is expensive or cheap?

In 2018, Willy Woo proposed NVT Signal values above 150 as overbought and under 45 as oversold. Historically, these figures worked well at identifying local peaks and troughs in Bitcoin’s Price. However, due to the changing nature of the Bitcoin network, a fixed fair value range of 45–150 may not be appropriate into the future.

Bitcoin is Constantly Evolving, and this Impacts its Fair Value

There are a number of reasons to believe that the fair value range of NVT Signal may not remain in a fixed band. The Bitcoin Network is constantly under development. Both via Bitcoin Core technical enhancements, and from the way Bitcoin’s surrounding infrastructure is engaged with and developed upon by the public. These developments significantly impact the transaction value transmitted on the Bitcoin network, and therefore alter the fair value of the NVT Signal.

What are some reasons why the fair value range of NVT Signal might change in the coming years?

NVT Signal’s fair value range might increase, because:

- Bitcoin is only 10 years old. It’s likely that relatively “high” and relatively “low” NVT Signal values will change with time, as have PE ratios in the stock market over the last century. For example, there are relatively fewer businesses with PE ratios below 15 today than there were 50–100 years ago.

- Increasing use of off-chain transactions. Some transactions are now made off-chain, including Liquid Network’s private side-chain which is used by many major exchanges such as BitFinex and BitMex. If the trend towards side-chains and private transactions continues, we can expect less-and-less transactions to be captured in the public on-chain data (reducing the relative value of the “T” in NVT). This could cause the fair value NVT range to increase with time.

NVT Signal’s fair value range might decrease, because:

- Bitcoin is like a start-up. It’s extremely volatile and its mainstream adoption and long-term success is far from certain. As young businesses can have extremely high PE ratios (they are traded at high prices in anticipation of growth and high future earnings), Bitcoin too may currently have an inflated NVT Signal range (in anticipation of increased transaction values in the future). Therefore, as Bitcoin matures, its long-term NVT Signal value could stabilize lower.

Based on the above, we can expect long-term trends in the NVT Signal fair value range to ebb and flow as the use case and technology infrastructure of Bitcoin matures. In fact, we have arguably already seen this change. If you believe the 84% drop in Bitcoin’s price to $3,150 in December 2018 was the low in the current market cycle, and consequently represented an “oversold” NVT Signal valuation, you would not have identified this using a NVT Signal range of 45 and lower. In December 2018, NVT Signal (using Blockchain.info data) did not drop below 70.

Establishing a Dynamic Range for the NVT Signal’s Fair Value

For the above reasons, a dynamic range is proposed for the NVT Signal fair value, which can be used to identify when Bitcoin is overbought or oversold.

The following range is proposed for assessing Bitcoin’s Fair value with NVT Signal:

- Overbought: NVT Signal > long-term mean +X * standard deviations

- Oversold: NVT Signal < long-term mean — Y * standard deviations

The above calculations are proposed to be performed over a rolling 2-year historical “look-back” period. In other words, at any point in time, only the prior 2 years’ worth of data should be considered in assessing relative value. This is roughly half the time between Bitcoin Supply halvings. In the future (in say, 5 years’ time plus), a 2-year look-back period is unlikely to be a sufficient window. Nonetheless, it was chosen here to give an ample period for historical review (8 years out of bitcoin’s short 10-year life); and because doubling the horizon to 4 years did not provide any measurable difference in the end results below.

Because Bitcoin’s NVT Signal is skewed (it has historically experienced more extreme highs than extreme lows),“X” and “Y” cannot be the same value …unless you never want to buy bitcoin again, or consider that it has never been cheap in its entire lifetime.

Today, the following defaults are proposed. Due to the reasons outlined below, these parameters should probably be reviewed every 2–4 years:

- Overbought: NVT Signal > 2-year mean +2.0 * standard deviations

- Oversold: NVT Signal < 2-year mean — 0.5 * standard deviations

Overbought is set here to 2 standard deviations above the mean. For a normally distributed data-set, this would mean Bitcoin is overbought roughly 2.5% of the time in any two year period. Though it turns out to be a somewhat higher percentage of the time given Bitcoin’s NVT Signal has not been normally distributed.

Oversold is considered anything less than 0.5 standard deviations below mean. Again, this is due to the NVT Signal’s skewness. For example, in the last 10 years, Bitcoin has never had an NVT Signal below mean less 2 standard deviations. Using 0.5 captures the December 2018 low of $3,150 as “oversold”.

A benefit of using the Dynamic Range NVT Signal is its interoperability across data sources. It is a know fact that estimates of “transaction value” differ across data vendors, as outlined by CoinMetrics here. This is due to the way Bitcoin issues “change” for transactions. Data vendors have their own process for estimating the “real transaction value”, and often come up with greatly different figures. Nonetheless, using a Dynamic Range for fair valuation with NVT signal should yield the same result of relative over- or under-valuation across different data sources. A fixed fair value NVT Signal band will not. This is because of the relativity of the dynamic range to the data observed.

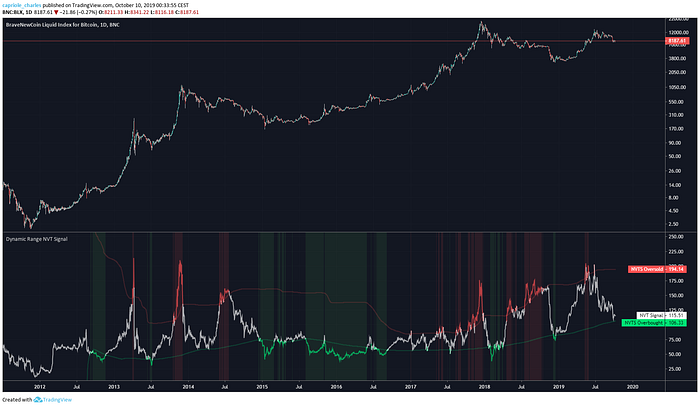

Bitcoin’s Dynamic Range NVT Signal Fair Value

Here are the results.

The white NVT Signal line turns red when it above the red overbought line, and green when below the green oversold line. The indicator fills red and green respectively to highlight these changes through time. As with traditional fixed band NVT Signal valuation, NVT Signal is generally more precise at identifying market tops than bottoms.

Based on the above default Dynamic Range settings, Bitcoin is currently fairly valued today and near “oversold” territory.

You can also check out the live indicator on TradingView here. If you don’t agree with any of the dynamic range settings used in this article, feel free to easily adjust them on TradingView and see the impact.

Considerations

The NVT Signal with a dynamic fair value range must be used with care.

As with all markets, an asset can remain “expensive” or “cheap” for extended periods or time and continue to get even more expensive or cheaper. This can be seen above during the 2015 -2016 period where NVT Signal spent much of the time ranging between 40 and 45. Arguably, this was the longest period of undervaluation (relative to actual use) in Bitcoin’s history.

As noted above, it is likely that a 2-year “look back period” for calculating mean and standard deviation will not be sufficient in the years to come. As Bitcoin matures and stabilizes (some time in the future), a longer “look back period” should probably be used. Further, with maturity Bitcoin’s NVT skewness may reduce, requiring adjustment in the “X” and “Y” values above. Nonetheless, to minimize the impact of over-fitting, it is recommended these parameters be reviewed no more than once every 2 years.

Finally, as Bitcoin ages, the validity of NVT Signal in general will need to be monitored. Particularly with respect to the potential for increasing use off-chain and private transactions which may diminish the validity of NVT.

Live Indicator on TradingView.

Disclaimer on Backtests

Any Backtest performance returns presented represent hypothetical returns and are meant to simulate how a strategy would have performed during the period shown had the strategy been implemented during that time. Backtested/simulated performance returns are hypothetical and do not reflect trading in actual accounts. Backtest returns are provided for informational purposes only to indicate historical performance had the strategy been implemented over the relevant time period. Backtested performance results have inherent limitations as to their relevance and use. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading, such as the ability to withstand losses or to adhere to a particular trading program in spite of trading losses, all of which can also adversely affect actual trading results. There are numerous other factors related to the markets in general and to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results, all of which can adversely affect actual trading results. Any and all of these factors mean that no representation is being made that strategies presented here will achieve performance similar to that shown, and in any case, past performance is no guarantee of future performance.