Welcome to Capriole’s Newsletter Update #59. A consolidation of the most important Bitcoin news, technicals and fundamentals.

Upside Surprises

The data reviewed below is very important, however there are a number of triggers which could shift things dramatically over the coming months which did not exist in prior cycles. For example, if the US Bitcoin Strategy Reserve (BSR) initiates any form of Bitcoin buying, we expect a huge and aggressive global response to do the same. A BSR would also result in a new, and the most important, long-term holder: the USA. The game theory of the US owning and growing a reserve of Bitcoin is not to be understated. Already many other countries are talking about a possible Bitcoin reserve at the government level including; Russia, Germany and Hong Kong (China). While it is early days, anything decisive on this front would negate any mid- or late-cycle narrative this year for Bitcoin and could extend the current cycle by years (like the Gold analogy discussed below). Furthermore, we also have a stream of probably pro-crypto legislation and initiatives coming out of the US in 2025. While an aggressive BSR is not our base case for 2025; it’s pretty clear that anything positive and unexpected in this regard will trigger a ginormous wave of long-term buying activity in Bitcoin. Whether or not it is this cycle is to be determined, but we expect it will happen eventually.

Whenever it is that the US initiates some form of active Bitcoin buying, all bets are off and such an event would likely have an effect similar to restarting the entire Bitcoin cycle from that point in time. It’s for these reasons that we see the potential for uncertainty and market surprises to be skewed positively to the upside for 2025 and we remain open minded to the various ways in which this cycle could play out.

In the last days alone, several events have occurred which have increased the odds of a BSR:

- Trump launched an $80B memecoin

- His sons were buying tens of millions of dollars of Bitcoin and altcoins through World Liberty Financial on inauguration day

- Saylor met with entire Trump cabinet just days ago

- Senator Lummis tweeted about a BSR discussion with Eric Trump today

On 18 January 2025, 2 days before his inauguration, Trump launched his memecoin (pictured above). The TRUMP meme quickly rallied to a fully diluted value of over $80B within 24 hours. This represents many multiples of Trump’s net worth from his entire life’s worth of Business ventures. We can debate the sustainability of the valuation of the TRUMP meme all day, but one thing is for sure: this is a world first and a striking step towards embracing the crypto industry by the president of the U.S.A. This move emboldens the legal status of digital assets and further incentivizes investors to embrace digital asset

Macro Recap

As Bitcoin continues to integrate into traditional financial markets, key data to monitor increasingly becomes macroeconomic. At a two-trillion-dollar market capitalization, Bitcoin is more affected by macro markets, equities, Federal Reserve and US government decisions today than ever before. Just a few years ago, Bitcoin didn’t even flinch during presidential elections. But today macro events drive major Bitcoin price movements, just as we saw with the November election, as our industry deepens its integration with traditional finance and equity markets.

Capriole has always utilized macroeconomic and equities data for our Bitcoin investment decision making. We were one of the first crypto funds and investors to do so in the industry and have found it invaluable for many years. Macro and equities data also forms the basis of our machine learning Macro Index strategy (original model article here), which we have been running live since 2022. This strategy summarises our view of Bitcoin as a macro asset and it is a strategy that has grown in importance in our portfolio. Macro Index now integrates into and informs our other strategies, including Trend King (now OneAI), altcoins and equities.

We see macro data and policy shifts as the key element to monitor in 2025, which is exactly why our last update centered on a macro analysis. Long story short – the macro outlook with the information we have today looks very strong for 2025. That said, there are a lot of unknowns. Significant potential policy shifts both good and bad could occur this year, especially in the next few months under a new presidency. On net, we believe the risk of new policy changes is skewed to the upside (positive), but we are open minded to all outcomes.

For example, a lot of the social space has filled with fear over the last weeks, largely driven by the 10 year treasury rallying and risk markets pulling back in early 2025. If you have been following our content, we held a different view and saw the dip in equities as largely a short-term opportunity, because:

- The S&P Put Call ratio reached the Covid 2020 extremes (a strong buy signal)

- Stock-to-Bond volatility suggests the macro trend is still risk on

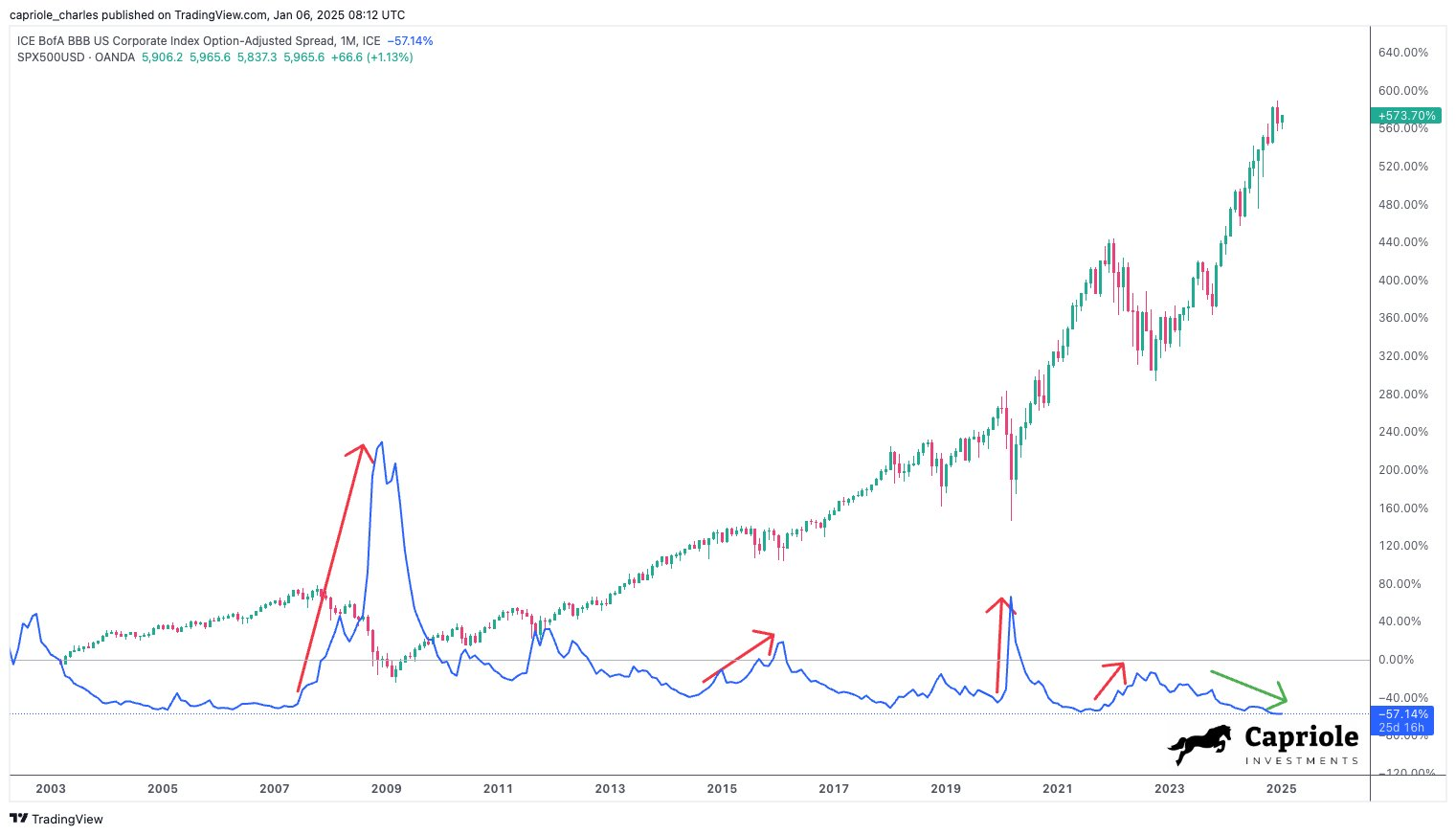

- Perhaps most importantly, credit spreads are still favouring more risky corporate debt over safer treasuries

Of course all data points can change at any time, but so far, it’s been a green light.

When corporate BBB credit spreads contract, it gives a strong signal that bond markets are still very much tilted to risk-on, a historically important macro indicator.

Given the positive macro environment, the next layer down we will discuss here is the broader Bitcoin cycle and what on-chain data is telling us today.

The Gold Comparable

One analogy we like, and have referenced before, is the Gold ETF launch. Following the Gold ETF launch, Gold consolidated at its 1980 all time high (ATH), much like Bitcoin was doing in mid-2024 in the $60-70K region following its ETH launches. Furthermore, the volatility behaviour we saw in Gold at its ATH was also mirrored in Bitcoin on all its key dips in 2024.

Following Gold’s ATH breakout, what followed for Gold was a 90% price rally in a relentless three year bull market.

A similar dynamic is quite possible for Bitcoin today. However, as Bitcoin is a much smaller asset, in a digital world, things tend to move more aggressively.

Gold following its ETF launch at its prior ATH in 2008-2010. We do not consider fractals like this to be useful forecasts, but it does give us perhaps the most comparable historic datapoint to Bitcoin today. In short, provided the political landscape is supportive of such a regime we think something like this dynamic is very possible. History does not repeat, but it does rhyme.

The Bitcoin Cycle

We often discuss the 12-18 months following each Bitcoin Halving as being the best performance window cyclically, driven by the change in supply dynamic and a reflexive regime that follows and ratchets prices higher. It’s in this window that 90% of Bitcoin’s historical returns historically occur and the opportunity for altcoin outperformance is highest. Based on this, we are currently bang in the middle of the optimal Bitcoin performance window on a time-wise basis. This suggests the real meat of the cycle, especially for altcoins (which saw their best performance in late 2017 and throughout 2021), is yet to come.

Based on prior cycle performance following the Halving, we may not have even set the floor for the next cycle bear market yet. Either way, the stage is set for a promising 2025 across crypto.

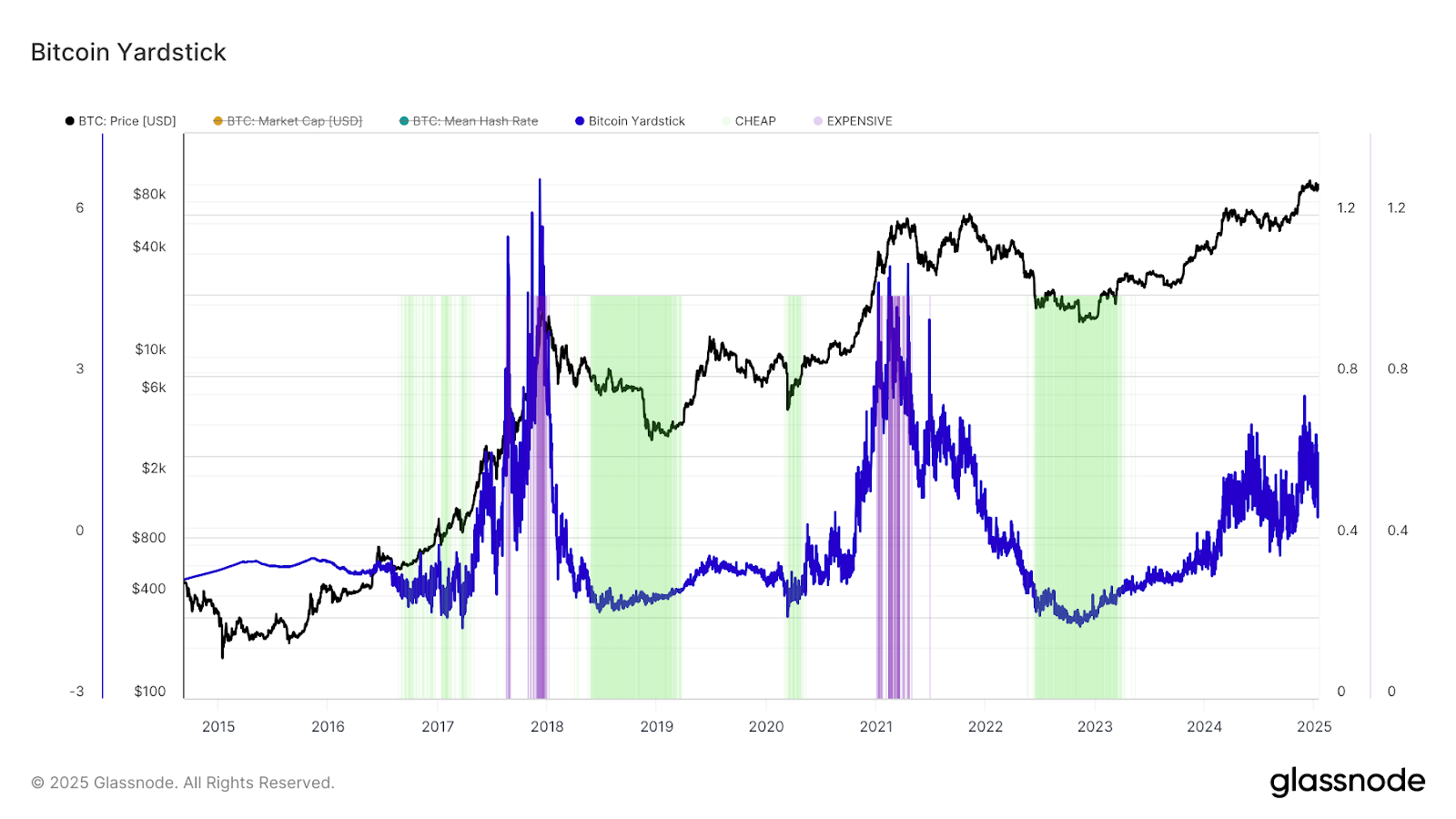

More broadly across on-chain data, many metrics suggest we are mid-cycle, including the Bitcoin Yardstick. We know we are not trading in the deep value region, and haven’t for some time, but historically much of Bitcoin’s returns come in the momentum, mid-phase of the cycle that we recently entered.

The Bitcoin Yardstick values Bitcoin against its hash-rate, based on this metric, we are mid-cycle.

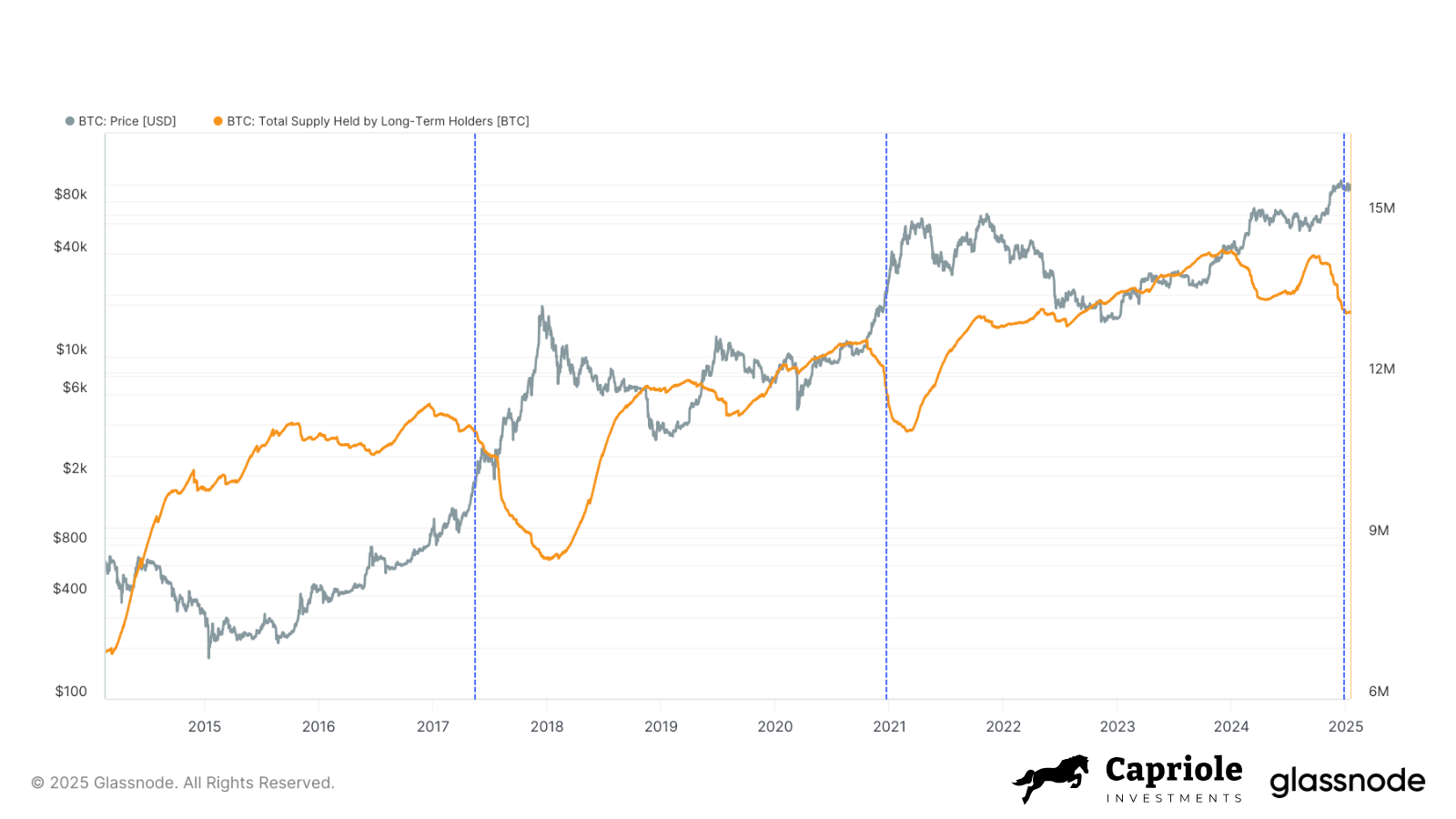

Long-term holder supply is a metric that forms the basis of many powerful on-chain indicators. It tells us how much of the total Bitcoin supply is in long-term investor wallets (coins held for more than half a year) and who statistically have a high likelihood of holding their coins long-term. This metric also tells us we are similarly placed today to early 2017 and early 2021. At these relative points in the prior cycles, the majority of the Bitcoin upside relative to the prior ATH was yet to come.

In the case of 2021, we did see a major drawdown in the middle of the year, this was triggered by the China mining ban which saw 50% of Bitcoin’s mining industry turn off overnight, resulting in a 50% drop in Bitcoin’s price. This was a catastrophic industry event which is unlikely to occur again. Nonetheless, full year 2021 still saw strong Bitcoin returns and the returns were even better for altcoins.

From similar points in LTH supply decline in prior cycles to today, Bitcoin saw its biggest cycle returns from the prior ATH. From this point onwards, altcoins performed even better.

This is a small selection of on-chain data points, but summarises the holistic view we see today. In future issues of the Capriole Newsletter, we will dive into Bitcoin on-chain metrics further.

Technicals

Finally technicals. We will keep it very simple this issue. Bitcoin is currently in price discovery. All major timeframes look strong. The below daily chart shows we are currently consolidating above the Daily (and Weekly) range, near all time highs. This can be interpreted a few ways, including as a Wyckoff re-accumulation consolidation before a new breakout leg emerges. In short, this chart continues to look bullish as long as Bitcoin keeps closing above $99K.

The Bottom-line

The Trump presidency has kickstarted a wave of speculation about a possible Bitcoin Strategic Reserve and other catalytic events. While the depth of it remains uncertain, recent and rapid fire news in the last days suggests a growing likelihood of something tangible brewing.

January’s macro position is very supportive of risk-on assets for 2025, a theme we have been pressing through Bitcoins dip to $89K and the S&P 500 drop to 5700. Bitcoin on-chain data suggests we are about half way through the cycle and cyclicals, seasonality and other comparables to prior Bitcoin cycles (and to Gold) suggest the meat of this cycle’s returns could very well still be ahead of us.

Charles Edwards

One Response

Could I see performance since 2020?